{kind=link}

Introduction

A balance sheet is one of the most important financial statements that shows the financial position of a business at a specific point in time. It presents what a business owns, what it owes, and the value left for the owner. In simple terms, it answers a very practical question: is the business financially healthy or not?

At its core, a balance sheet is built on a simple idea. Everything a business owns, known as assets, is funded either by borrowing money, called liabilities, or by the owner’s investment, known as equity. When recorded correctly, both sides always match, which is why it is called a balance sheet.

For example, imagine a small shop owner who has cash of 5,000, inventory worth 3,000, and equipment valued at 2,000. The total assets are 10,000. If the owner has a bank loan of 4,000 and has invested 6,000 of personal money, the balance sheet will look like this:

| Category | Amount |

|---|---|

| Assets | 10,000 |

| Liabilities | 4,000 |

| Equity | 6,000 |

This simple structure helps business owners, investors, and accountants quickly understand where the money is coming from and how it is being used.

Some key points to understand

• A balance sheet shows the financial position at a specific date

• It helps in making better business decisions

• It is used by investors and lenders to assess risk

• It ensures financial records are accurate and complete

A clear understanding of the balance sheet allows even beginners to take control of their finances and make informed decisions with confidence.

Key Components of a Balance Sheet

A balance sheet is built around three main components that work together to show the complete financial picture of a business. Understanding these components clearly is the first step toward mastering financial statements.

Assets

Assets represent everything a business owns that has value and can provide future benefits. These are usually divided into two categories

• Current assets which can be converted into cash within one year such as cash, inventory, and accounts receivable

• Non current assets which are long term resources such as machinery, buildings, and equipment

For example, if a business has cash of 2,000, inventory of 3,000, and equipment worth 5,000, all of these are recorded as assets because they contribute to business operations.

Liabilities

Liabilities are the obligations or debts that a business needs to pay in the future. These also fall into two categories

• Current liabilities such as short term loans, unpaid bills, and accounts payable

• Long term liabilities such as bank loans or mortgages that are paid over several years

For instance, if a company owes 1,500 to suppliers and has a long term loan of 4,000, both amounts are liabilities because they represent money owed to others.

Equity

Equity represents the owner’s share in the business after all liabilities are deducted from assets. It shows the net worth of the business and reflects the owner’s investment and retained profits.

If a business has total assets of 10,000 and total liabilities of 5,000, the equity will be 5,000. This means the owner’s claim in the business is equal to that amount.

| Component | Meaning | Example |

|---|---|---|

| Assets | What the business owns | Cash, inventory |

| Liabilities | What the business owes | Loans, payables |

| Equity | Owner’s share or net worth | Capital, profit |

A clear understanding of these three components makes it easier to read, prepare, and analyze a balance sheet with confidence.

Balance Sheet Formula Explained

At the heart of every balance sheet is a simple but powerful formula that keeps the entire statement accurate and structured. This formula ensures that everything a business owns is properly accounted for.

Assets=Liabilities+Equity

This equation means that all assets of a business are financed either through liabilities or equity. In other words, a business does not acquire resources out of nowhere. Every asset has a source of funding.

Understanding the Formula

• Assets are resources like cash, inventory, and equipment

• Liabilities are obligations such as loans and unpaid bills

• Equity represents the owner’s investment and retained profits

The formula must always stay balanced. If one side changes, the other side must adjust accordingly.

Simple Example

Suppose a business has the following

| Category | Amount |

|---|---|

| Assets | 20,000 |

| Liabilities | 8,000 |

| Equity | 12,000 |

Here, total assets of 20,000 are equal to liabilities plus equity, which is also 20,000. This confirms that the balance sheet is correct.

How It Works in Real Life

If a business takes a loan of 5,000, both assets and liabilities increase by 5,000 because cash comes in and a debt is created.

If the owner invests additional money, assets and equity increase.

If the business earns profit, equity increases through retained earnings.

Key Points to Remember

• The formula is the foundation of accounting

• It always stays balanced

• Every financial transaction affects at least two components

• It helps detect errors in financial records

A clear understanding of this formula makes it much easier to prepare and analyze a balance sheet with confidence.

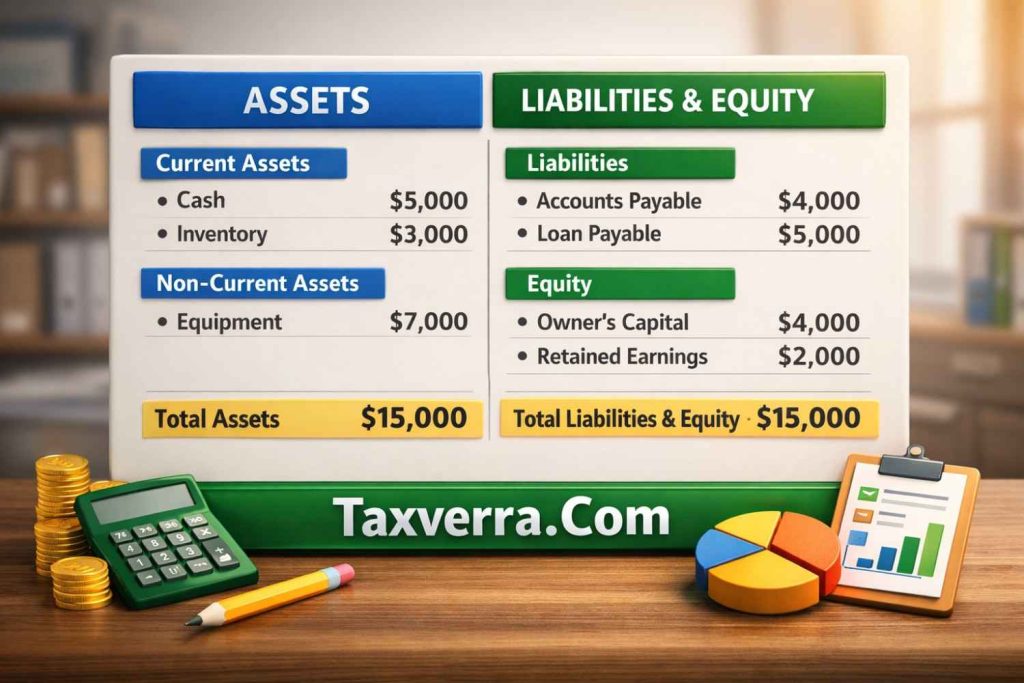

Standard Balance Sheet Format

A standard balance sheet format presents financial information in a clear and structured way so that anyone can quickly understand a company’s financial position. It is usually divided into two main sections: assets on one side and liabilities and equity on the other.

The format can be presented in two common styles. The vertical format is widely used in reports, where items are listed from top to bottom. The horizontal format places assets on the left and liabilities with equity on the right.

Basic Structure

A typical balance sheet follows this order

Assets

• Current assets

• Non current assets

Liabilities

• Current liabilities

• Long term liabilities

Equity

• Owner’s capital

• Retained earnings

Example of a Simple Balance Sheet Format

This format ensures that total assets match the sum of liabilities and equity, maintaining the balance.

Key Features of the Standard Format

• Items are grouped into logical categories for clarity

• Short term and long term elements are separated

• Totals are clearly calculated and presented

• The final totals must always match

A well structured balance sheet format not only improves readability but also helps in accurate financial analysis and decision making.

Step-by-Step Guide to Prepare a Balance Sheet

Preparing a balance sheet becomes simple when you follow a clear and organized process. It helps you accurately record what a business owns, owes, and the owner’s financial interest at a specific date.

Step 1: Collect Financial Information

Start by gathering all financial records such as cash books, bank statements, invoices, loan details, and inventory records. Accurate data is the foundation of a correct balance sheet.

Step 2: List All Assets

Identify everything the business owns and classify them into:

• Current assets like cash, bank balance, inventory, and receivables

• Non current assets like equipment, furniture, and buildings

Make sure each item is valued correctly.

Step 3: Record All Liabilities

Next, list everything the business owes:

• Current liabilities such as unpaid bills and short term loans

• Long term liabilities like bank loans or mortgages

This shows the financial obligations of the business.

Step 4: Calculate Owner’s Equity

Equity is calculated using the balance sheet formula:

Assets minus Liabilities equals Equity

It includes owner’s capital and retained earnings.

Step 5: Arrange in Standard Format

Organize everything in a proper structure:

• Assets on one side or top section

• Liabilities and equity on the other side or below

Ensure totals are clearly mentioned.

Step 6: Verify the Balance

Check that total assets are equal to liabilities plus equity. If both sides match, your balance sheet is correct.

Example Summary

| Item | Amount |

|---|---|

| Total Assets | 50,000 |

| Total Liabilities | 20,000 |

| Equity | 30,000 |

Final Tip

Always double check figures and update records regularly to maintain accuracy and financial clarity.

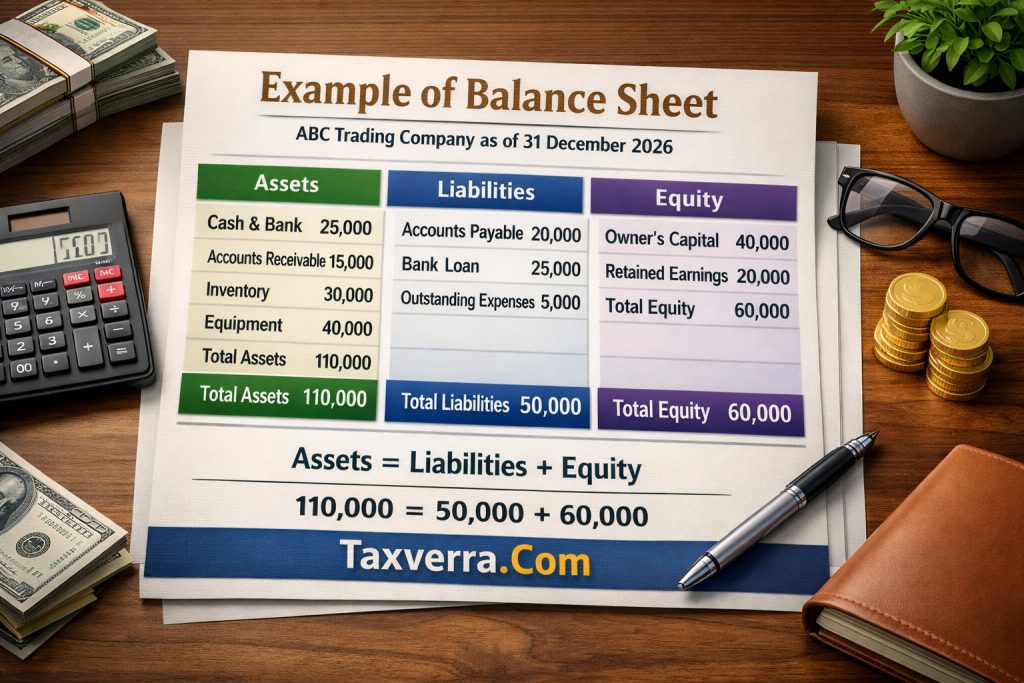

Real-Life Balance Sheet Example (ABC Trading Company)

A balance sheet is one of the most important financial statements used by businesses to understand their financial position at a specific point in time. It shows what a company owns, what it owes, and the remaining value belonging to the owner. In simple terms, it helps answer whether a business is financially strong or weak.

A real life example can be seen in a small trading business such as ABC Trading Company. This company prepares its balance sheet at the end of the year to evaluate performance and financial stability.

Example of Balance Sheet

Key insights from this example

• Cash and inventory show how much liquid and stock value the business holds

• Loans and payables represent obligations that must be settled

• Owner equity shows the true value remaining for the business owner after debts

This example highlights how a balance sheet provides a clear financial snapshot. Investors and business owners use it to make decisions about expansion, borrowing, and cost control. A strong balance sheet usually means higher liquidity, manageable debt, and healthy growth potential.

How to Read and Understand a Balance Sheet

Understanding a balance sheet becomes much easier when you know what each section represents and how they work together. A balance sheet is a financial statement that shows a company’s assets, liabilities, and equity at a specific point in time. It follows a simple rule that keeps everything balanced.

The key idea is the accounting equation: Assets = Liabilities + Equity. This equation helps you see whether the company is financially stable and how its resources are financed.

How to read a balance sheet step by step

Start with assets, which are everything the business owns. These are usually divided into current assets like cash and inventory and non current assets like equipment or buildings. Higher assets generally indicate stronger financial capacity.

Next look at liabilities, which represent what the business owes to others. These include bank loans, unpaid bills, and other obligations. If liabilities are too high compared to assets, it may signal financial pressure.

Then examine equity, which is the owner’s share in the business after liabilities are deducted. It includes capital invested and retained earnings. Strong equity means the business has built value over time.

Simple structure example

| Section | What it shows | Example items |

|---|---|---|

| Assets | What the business owns | Cash, inventory, equipment |

| Liabilities | What the business owes | Loans, payables |

| Equity | Owner’s remaining value | Capital, retained profit |

Key points to remember

• Always compare assets with liabilities to understand risk

• Check liquidity by looking at cash and receivables

• Review equity to see long term business strength

• A balanced sheet means the accounting equation is correctly applied

In short, reading a balance sheet helps you understand whether a business is growing, stable, or facing financial challenges.

Basic Balance Sheet Analysis

A balance sheet is a financial statement that shows what a business owns, what it owes, and the remaining value for owners at a specific point in time. Basic balance sheet analysis helps understand the financial health, liquidity, and stability of a company by studying its core parts: assets, liabilities, and equity.

At its simplest, the balance sheet follows the equation: Assets = Liabilities + Equity. This means everything a business owns is financed either by debt or by the owner’s investment.

A basic analysis focuses on whether the business has enough current assets such as cash and receivables to cover its current liabilities like short term loans and payables. It also checks how efficiently long term resources are being used.

For example, if a small business has strong cash reserves but very high short term debt, it may face liquidity pressure even if it looks profitable on paper. On the other hand, a balanced structure indicates stability and lower financial risk.

Key Points in Basic Analysis

- Check liquidity position by comparing current assets and current liabilities

- Evaluate debt level to understand financial risk

- Review owner’s equity to see long term stability

- Compare assets growth over time for performance trends

Simple Example

| Category | Amount (USD) |

|---|---|

| Cash | 10,000 |

| Inventory | 5,000 |

| Total Assets | 15,000 |

| Liabilities | 6,000 |

| Equity | 9,000 |

In this example, the business has more assets than liabilities, showing a healthy financial position.

Overall, basic balance sheet analysis helps investors, owners, and managers make better decisions by clearly showing financial strength and risk level.

Common Balance Sheet Mistakes to Avoid

A balance sheet is one of the most important financial statements, but many businesses make errors that lead to wrong decisions and weak financial planning. Understanding common mistakes helps improve accuracy, reliability, and financial control.

One of the most frequent mistakes is incorrect classification of items. Businesses sometimes record short term loans as long term liabilities or mix operating expenses with capital assets. This distorts the real financial position and misleads decision makers.

Another common issue is failing to update records regularly. When transactions are not recorded on time, the balance sheet does not reflect the true financial condition of the business. This can lead to cash flow surprises and budgeting problems.

Many small businesses also ignore depreciation adjustments. Assets like machinery and vehicles lose value over time, and not recording depreciation results in inflated asset values.

Errors in inventory valuation are also common. Overstated inventory increases assets artificially, while understated inventory hides actual business value.

Key Mistakes to Avoid

- Misclassification of assets and liabilities

- Delayed or incomplete recording of transactions

- Ignoring depreciation of fixed assets

- Incorrect inventory valuation

- Not reconciling bank balances regularly

Example of a Common Error

| Item | Correct Treatment | Common Mistake |

|---|---|---|

| Loan (2 years) | Non current liability | Recorded as current liability |

| Equipment | Asset with depreciation | Shown at original cost only |

| Inventory | Actual counted value | Estimated or outdated value |

Another serious mistake is not reconciling bank statements, which can create hidden discrepancies between recorded and actual cash.

In conclusion, avoiding these common balance sheet mistakes ensures more accurate financial reporting. It helps businesses make better investment decisions, manage risk effectively, and maintain long term financial stability.

Balance Sheet for Small Business Owners

A balance sheet is a key financial statement that helps small business owners understand their financial position at a specific point in time. It shows what the business owns, what it owes, and the remaining value for the owner. This information is essential for making smart decisions about spending, borrowing, and growth.

For small businesses, the balance sheet is especially important because it highlights cash flow strength, debt levels, and overall business stability. Many small business owners focus only on profit, but the balance sheet reveals whether the business can actually meet its short term and long term obligations.

The basic structure includes assets, liabilities, and equity. Assets include cash, inventory, and equipment. Liabilities include loans and unpaid bills. Equity represents the owner’s share after all liabilities are deducted.

Key Points for Small Business Owners

- Monitor cash position regularly to avoid liquidity issues

- Keep track of short term liabilities like supplier payments

- Review inventory levels to avoid overstocking or shortages

- Understand loan obligations and repayment schedules

- Check owner’s equity to measure long term growth

Simple Example of a Small Business Balance Sheet

| Category | Amount |

|---|---|

| Cash | 8,000 |

| Inventory | 4,000 |

| Equipment | 6,000 |

| Total Assets | 18,000 |

| Liabilities | 7,000 |

| Owner’s Equity | 11,000 |

In this example, the business has more assets than liabilities, showing a stable financial position.

For small business owners, regularly reviewing the balance sheet helps identify risks early and supports better planning. It also improves confidence when applying for loans or attracting investors. A clear understanding of the balance sheet leads to stronger financial control and long term business success.

Tools & Templates for Balance Sheet

Creating a balance sheet becomes much easier when small business owners and accountants use the right tools and templates. These resources help maintain accuracy, speed, and consistency in financial reporting, especially when managing multiple transactions.

Today, businesses do not need to build balance sheets manually. Many digital accounting tools automatically generate balance sheets by recording daily income, expenses, assets, and liabilities. This reduces human error and saves valuable time.

Some widely used tools include spreadsheet software like Excel and Google Sheets, as well as accounting platforms such as QuickBooks, Xero, and Zoho Books. These tools offer ready made templates that can be customized based on business size and industry needs.

A good balance sheet template usually includes structured sections for current assets, fixed assets, current liabilities, long term liabilities, and owner’s equity. It also ensures that totals are automatically calculated using formulas.

Key Tools and Templates

- Excel balance sheet templates for manual customization

- Google Sheets templates for cloud based access and sharing

- QuickBooks automated financial statements

- Xero accounting templates for real time reporting

- Zoho Books templates for small business accounting

Example of a Simple Template Structure

| Section | Description |

|---|---|

| Current Assets | Cash, receivables, inventory |

| Fixed Assets | Equipment, vehicles, property |

| Current Liabilities | Bills, short term loans |

| Long Term Liabilities | Bank loans, mortgages |

| Owner’s Equity | Remaining business value |

For example, a small retail business can use Excel to track daily sales and automatically update its balance sheet at the end of each month. This helps owners quickly see whether the business is growing or facing financial pressure.

In conclusion, using the right tools and templates simplifies balance sheet preparation and improves financial decision making. It allows business owners to focus more on growth while ensuring their financial records remain clear and accurate.

Frequently Asked Questions (FAQs)

1. What is a balance sheet?

A balance sheet is a financial statement that shows assets, liabilities, and owner’s equity of a business at a specific date. It reflects what the business owns and owes.

2. Why is a balance sheet important?

It provides a clear picture of financial health, stability, and liquidity. Banks and investors use it to assess whether a business is financially safe.

3. What are the main parts of a balance sheet?

The three main parts are assets, liabilities, and equity. Assets are what the business owns, liabilities are what it owes, and equity is the owner’s remaining value.

4. How often should a balance sheet be prepared?

It is usually prepared monthly, quarterly, or yearly depending on business size. Regular preparation helps track financial progress.

5. What is included in assets?

Assets include cash, bank balance, inventory, accounts receivable, equipment, and property.

6. What are liabilities in simple terms?

Liabilities are financial obligations or debts such as loans, unpaid bills, and taxes payable.

7. What is owner’s equity?

Owner’s equity is the residual value of the business after liabilities are deducted from assets. It represents the owner’s share.

8. What is the balance sheet formula?

The formula is:

Assets = Liabilities + Equity

9. Can a balance sheet show profit or loss?

No, profit or loss is shown in the income statement, but retained earnings in equity reflect accumulated profits.

10.What is a classified balance sheet?

It is a balance sheet that separates items into current and non current categories for better analysis.

11. What is the difference between current and fixed assets?

Current assets are short term items like cash and inventory, while fixed assets are long term items like machinery and buildings.

12. Why does a balance sheet need to balance?

Because every asset is financed either by debt or owner investment, ensuring both sides always remain equal.

Conclusion

A balance sheet is one of the most important financial statements for understanding the true financial position of a business. It provides a clear view of what the business owns, what it owes, and the value remaining for the owner. By analyzing it properly, businesses can measure their stability, liquidity, and long term strength.

For small business owners, the balance sheet is not just an accounting requirement but a practical tool for decision making. It helps identify whether the business can manage short term expenses, handle debt obligations, and support future growth. When reviewed regularly, it becomes easier to spot financial risks early and take corrective actions.

A strong balance sheet reflects healthy cash flow, controlled liabilities, and growing assets. On the other hand, weaknesses such as high debt or poor asset management can signal potential financial pressure. This makes consistent review and accurate recording extremely important.

In simple terms, the balance sheet acts like a financial health report card for any business. It supports better planning, improves investor confidence, and helps owners stay in control of their finances.

Overall, understanding and maintaining a balance sheet properly leads to better financial discipline, smarter business decisions, and long term success.