{kind=link}

Introduction

A cash flow statement shows how money actually moves in and out of a business over a period of time. While profits are important, they do not always reflect the real financial position. A company can report strong profits but still face cash shortages if it cannot collect payments on time or manages expenses poorly. This is why understanding cash flow is essential for both businesses and individuals.

At its core, the cash flow statement focuses on liquidity, which means the ability to meet short term obligations. It helps business owners, investors, and accountants see whether a company can pay its bills, invest in growth, and handle unexpected expenses without financial stress.

Example:

A company reports a profit of 50,000. However, most sales were made on credit and customers have not paid yet. At the same time, the company must pay salaries and suppliers in cash. Even with profit, the business may struggle to operate due to lack of cash.

Why Cash Flow Matters:

- Ensures business survival by maintaining enough cash for daily operations

- Supports better decision making for investments and expenses

- Helps identify financial problems early before they become serious

- Builds confidence for investors and lenders

Profit vs Cash Flow (Simple View):

| Aspect | Profit | Cash Flow |

|---|---|---|

| Meaning | Earnings after expenses | Actual cash movement |

| Based on | Accounting rules | Real cash transactions |

| Impact | Shows performance | Shows liquidity |

In simple terms, profit shows how well a business is performing, but cash flow shows whether it can survive and grow. This makes the cash flow statement one of the most practical and powerful financial tools.

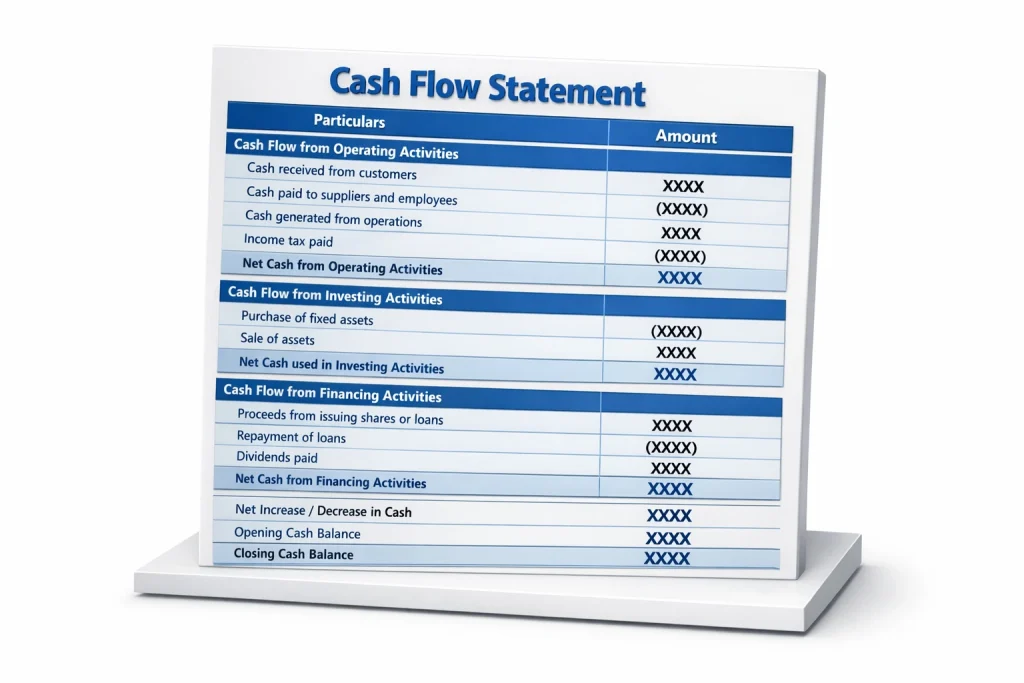

What is a Cash Flow Statement?

A Cash Flow Statement is a financial report that shows how cash moves in and out of a business during a specific period. Unlike profit, which includes non-cash items, this statement focuses only on actual cash transactions. It helps businesses understand whether they have enough liquidity to meet daily expenses, pay debts, and invest in growth.

The statement is divided into three main sections:

• Operating Activities

Cash generated from core business operations such as sales, payments to suppliers, and salaries.

Example: A company receives cash from customers and pays rent and wages.

• Investing Activities

Cash used for buying or selling long-term assets like equipment, land, or investments.

Example: Purchasing machinery or selling an old building.

• Financing Activities

Cash related to funding the business through loans, equity, or dividends.

Example: Taking a bank loan or paying dividends to shareholders.

Simple Example:

A small business earns 50,000 from customers, pays 30,000 in expenses, buys equipment worth 10,000, and takes a loan of 5,000. The cash flow statement shows how these activities affect the final cash balance.

Summary Table:

| Section | Cash Inflow Example | Cash Outflow Example |

|---|---|---|

| Operating Activities | Cash from customers | Salaries, rent |

| Investing Activities | Sale of equipment | Purchase of assets |

| Financing Activities | Loan received | Loan repayment, dividends |

Why it matters:

A business can be profitable but still face cash shortages. The cash flow statement highlights real cash position, making it easier for managers, investors, and creditors to make informed decisions.

Importance of Cash Flow Statement in Financial Analysis

The Importance of a Cash Flow Statement in Financial Analysis lies in its ability to show the real movement of cash within a business. While profit figures may look strong, they do not always reflect actual cash availability. This statement provides a clear picture of how well a company manages its cash to sustain operations and grow.

One of the key reasons it is important is that it helps assess liquidity. A company may report high profits but still struggle to pay its short-term obligations. By analyzing cash inflows and outflows, analysts can determine whether the business has enough cash to meet expenses like salaries, rent, and loan payments.

It also plays a major role in evaluating financial flexibility. Investors and managers use it to understand how easily a company can adapt to unexpected situations, invest in new opportunities, or handle economic downturns.

Another important aspect is identifying the quality of earnings. If profits are high but operating cash flow is low, it may indicate issues such as delayed customer payments or aggressive accounting practices. Strong operating cash flow usually signals a healthy and sustainable business.

Key Benefits in Financial Analysis:

• Helps in evaluating liquidity and solvency

• Shows the ability to generate cash from core operations

• Assists in investment decision-making

• Highlights cash management efficiency

• Detects potential financial risks

Example:

A company reports a profit of 100,000 but its cash flow from operating activities is only 20,000. This signals that most sales are on credit, and the company might face cash shortages despite being profitable.

Quick Overview Table:

| Aspect | Role of Cash Flow Statement |

|---|---|

| Liquidity | Ensures ability to pay short-term debts |

| Profit Quality | Verifies if profits are backed by cash |

| Investment Decisions | Helps evaluate expansion opportunities |

| Risk Analysis | Identifies potential cash shortages |

In financial analysis, the cash flow statement acts as a reality check. It connects profit with actual cash, helping stakeholders make smarter and more reliable decisions.

Components of a Cash Flow Statement

The Components of a Cash Flow Statement explain how cash enters and leaves a business. These components help users understand the company’s financial strength, cash position, and operational efficiency. The statement is divided into three main sections, each focusing on a different type of activity.

1. Operating Activities

This section shows cash flows from the company’s core business operations. It reflects how much cash is generated from regular activities like selling goods or providing services.

• Cash received from customers

• Cash paid to suppliers and employees

• Payment of taxes and interest

Example: If a business collects 80,000 from customers and pays 50,000 in expenses, the net cash flow from operating activities is positive.

2. Investing Activities

This part records cash used in or generated from buying and selling long-term assets. It shows how the company is investing in its future growth.

• Purchase of machinery, land, or equipment

• Sale of assets

• Investments in other businesses

Example: Buying equipment for 20,000 results in a cash outflow, while selling old machinery generates inflow.

3. Financing Activities

This section includes cash transactions related to funding the business. It shows how the company raises capital and returns value to investors.

• Issuing shares or taking loans

• Repayment of loans

• Payment of dividends

Example: Receiving a loan of 30,000 increases cash, while repaying debt reduces it.

Summary Table:

| Component | Cash Inflow Example | Cash Outflow Example |

|---|---|---|

| Operating Activities | Cash from customers | Salaries, rent, expenses |

| Investing Activities | Sale of assets | Purchase of equipment |

| Financing Activities | Loan, share capital | Loan repayment, dividends |

Why these components matter:

Each section provides a different insight. Operating activities show business sustainability, investing activities indicate growth strategy, and financing activities reveal how the business is funded.

Together, these components give a complete picture of how effectively a company manages its cash.

Cash Flow Statement Format (Standard Structure)

The Cash Flow Statement Format (Standard Structure) presents how cash flows are organized in a clear and consistent way. It helps users easily track where cash is generated and how it is spent during a specific period. The structure is divided into three main sections, followed by the net change in cash and the closing balance.

Key Highlights of the Format:

• The statement always starts with operating activities because they reflect core business performance

• Investing activities show long-term asset decisions

• Financing activities explain how the business is funded

• The final section reconciles opening and closing cash balances

Example:

If operating activities generate 40,000, investing activities use 15,000, and financing activities provide 10,000, the net increase in cash will be 35,000.

Why this format is important:

This structured layout ensures consistency across companies, making it easier for investors, analysts, and managers to compare financial performance and evaluate cash management efficiency.

In simple terms, the format answers three essential questions:

How much cash is generated, where it is spent, and what is the final cash position.

Methods of Preparing Cash Flow Statement

A Cash Flow Statement is an essential financial report that shows how cash moves in and out of a business. Preparing this statement helps management, investors, and creditors understand the company’s liquidity and operational efficiency. There are two main methods to prepare a cash flow statement: the Direct Method and the Indirect Method.

1. Direct Method

In the Direct Method, cash inflows and outflows from operating activities are recorded directly. This method lists all major cash receipts such as cash received from customers and cash paid to suppliers, employees, and other operating expenses. It provides a clear view of actual cash movements, making it easy to understand.

Example of Direct Method (Operating Activities)

| Particulars | Amount (USD) |

|---|---|

| Cash received from customers | 120,000 |

| Cash paid to suppliers | 50,000 |

| Cash paid to employees | 30,000 |

| Net cash from operations | 40,000 |

2. Indirect Method

The Indirect Method starts with net profit and adjusts it for non-cash transactions and changes in working capital. Common adjustments include depreciation, amortization, and changes in accounts receivable or payable. This method is widely used because it links the income statement with cash flows, making it easier for accountants to prepare.

Example of Indirect Method (Operating Activities)

| Particulars | Amount (USD) |

|---|---|

| Net profit | 50,000 |

| Add: Depreciation | 5,000 |

| Less: Increase in Accounts Receivable | 10,000 |

| Net cash from operations | 45,000 |

Both methods also include investing and financing activities but differ mainly in operating cash flow presentation. The choice of method depends on management preference, accounting standards, and the level of detail required for cash analysis.

By understanding these methods, businesses can make informed decisions about liquidity management, investment planning, and operational efficiency, ensuring sustainable growth.

Step-by-Step Guide to Prepare a Cash Flow Statement

A Cash Flow Statement tracks the movement of cash in a business, helping management, investors, and creditors assess liquidity and operational efficiency. Preparing it systematically ensures accuracy and clarity. Here’s a step-by-step guide:

Step 1: Decide the Method

Choose between the Direct Method or the Indirect Method for operating activities.

- Direct Method: Records actual cash receipts and payments.

- Indirect Method: Starts with net profit and adjusts for non-cash items and working capital changes.

Step 2: Gather Financial Data

Collect the Income Statement, Balance Sheets for current and previous periods, and records of cash transactions.

Step 3: Calculate Cash Flow from Operating Activities

- Direct Method Example:

| Particulars | Amount (USD) |

|---|---|

| Cash received from customers | 120,000 |

| Cash paid to suppliers | 50,000 |

| Cash paid to employees | 30,000 |

| Net cash from operations | 40,000 |

- Indirect Method Example:

| Particulars | Amount (USD) |

|---|---|

| Net profit | 50,000 |

| Add: Depreciation | 5,000 |

| Less: Increase in Accounts Receivable | 10,000 |

| Net cash from operations | 45,000 |

Step 4: Determine Cash Flow from Investing Activities

Include cash spent or received from buying or selling assets, such as machinery, land, or investments.

Step 5: Determine Cash Flow from Financing Activities

Include cash movements related to borrowing, repayment of loans, issuing shares, or paying dividends.

Step 6: Summarize Total Cash Flow

Add cash flows from operating, investing, and financing activities to calculate net increase or decrease in cash. Reconcile this with opening and closing cash balances.

Step 7: Review and Verify

Double-check all entries to ensure accuracy and compliance with accounting standards.

This step-by-step approach ensures a clear understanding of cash movements, helping businesses make informed financial decisions and maintain strong liquidity.

A Cash Flow Statement provides insight into how cash moves in and out of a business during a specific period. Here’s a practical example for a company, XYZ Ltd, for the year ending 2025, using the Indirect Method, which is widely preferred.

Step 1: Cash Flow from Operating Activities

Start with Net Profit and adjust for non-cash items and changes in working capital.

| Particulars | Amount (USD) |

|---|---|

| Net Profit | 60,000 |

| Add: Depreciation | 10,000 |

| Less: Increase in Accounts Receivable | 5,000 |

| Add: Increase in Accounts Payable | 3,000 |

| Net Cash from Operating Activities | 68,000 |

Step 2: Cash Flow from Investing Activities

Include purchases and sales of long-term assets.

| Particulars | Amount (USD) |

|---|---|

| Purchase of Machinery | (20,000) |

| Sale of Old Equipment | 5,000 |

| Net Cash Used in Investing Activities | (15,000) |

Step 3: Cash Flow from Financing Activities

Include cash received or paid for loans, dividends, or share capital.

| Particulars | Amount (USD) |

|---|---|

| Proceeds from Long-Term Loan | 25,000 |

| Dividend Paid | (10,000) |

| Net Cash from Financing Activities | 15,000 |

Step 4: Net Increase in Cash

| Particulars | Amount (USD) |

|---|---|

| Net Cash from Operating Activities | 68,000 |

| Net Cash from Investing Activities | (15,000) |

| Net Cash from Financing Activities | 15,000 |

| Net Increase in Cash | 68,000 |

| Opening Cash Balance | 20,000 |

| Closing Cash Balance | 88,000 |

This practical example shows that XYZ Ltd generated cash mainly through operating activities, while investing activities reduced cash. Financing activities helped by bringing additional funds.

A well-prepared cash flow statement like this enables management to assess liquidity, plan investments, and make strategic financial decisions.

Cash Flow Statement Analysis

Cash Flow Statement Analysis is the process of examining a company’s cash inflows and outflows to assess its financial health, liquidity, and ability to generate cash for operations, investments, and financing activities. Unlike the income statement, which records profits, the cash flow statement reveals the actual cash available to meet obligations.

1. Analyze Operating Activities

Operating cash flow indicates whether a business generates sufficient cash from its core operations. Positive operating cash flow is a sign of financial strength, while consistent negative cash flow may indicate operational problems.

Example:

| Particulars | Amount (USD) |

|---|---|

| Net Cash from Operating Activities | 68,000 |

| Net Profit | 60,000 |

| Analysis | Cash generated exceeds profit, indicating strong operational efficiency |

2. Analyze Investing Activities

Investing cash flow shows how much cash is used for or generated from long-term assets like property, plant, and equipment. Negative cash flow here is often a sign of expansion, while positive cash flow may indicate asset sales.

Example:

| Particulars | Amount (USD) |

|---|---|

| Purchase of Machinery | (20,000) |

| Sale of Old Equipment | 5,000 |

| Net Investing Cash Flow | (15,000) |

| Analysis | Cash outflow reflects investment in business growth |

3. Analyze Financing Activities

Financing cash flow reveals how a company funds its operations, through debt, equity, or dividends. Positive cash flow may indicate raising funds, while negative may indicate loan repayment or dividend payments.

4. Overall Analysis

By combining all three sections, one can determine the net increase or decrease in cash and assess the company’s liquidity position.

| Section | Net Cash (USD) |

|---|---|

| Operating Activities | 68,000 |

| Investing Activities | (15,000) |

| Financing Activities | 15,000 |

| Net Increase in Cash | 68,000 |

Conclusion: Cash flow analysis helps stakeholders understand where cash comes from, how it is used, and whether the business can sustain operations and growth. It is an indispensable tool for financial planning and decision-making.

Key Cash Flow Ratios

Cash Flow Ratios are financial metrics derived from the cash flow statement that help evaluate a company’s liquidity, operational efficiency, and financial stability. They are especially useful for investors, creditors, and management to understand how well a company generates and manages cash.

1. Operating Cash Flow Ratio

This ratio measures a company’s ability to cover its current liabilities using cash generated from operations.

Formula:

Operating Cash Flow Ratio = Cash from Operations ÷ Current Liabilities

Example:

If cash from operations is $68,000 and current liabilities are $40,000:

Operating Cash Flow Ratio = 68,000 ÷ 40,000 = 1.7

Interpretation: The company can cover its short-term obligations 1.7 times with its operating cash.

2. Cash Flow to Sales Ratio

This ratio indicates the proportion of cash generated from sales.

Formula:

Cash Flow to Sales = Cash from Operations ÷ Net Sales

Example:

Cash from operations = $68,000, Net sales = $200,000

Cash Flow to Sales = 68,000 ÷ 200,000 = 0.34 or 34%

Interpretation: 34% of sales are converted into actual cash.

3. Free Cash Flow (FCF)

Free Cash Flow represents the cash available after capital expenditures for business expansion, debt repayment, or dividends.

Formula:

Free Cash Flow = Cash from Operations − Capital Expenditures

Example:

Cash from operations = $68,000, Capital expenditures = $20,000

Free Cash Flow = 68,000 − 20,000 = $48,000

Interpretation: The company has $48,000 free to invest or distribute.

Summary Table of Key Ratios

| Ratio | Formula | Example | Interpretation |

|---|---|---|---|

| Operating Cash Flow Ratio | Cash from Operations ÷ Current Liabilities | 1.7 | Strong liquidity |

| Cash Flow to Sales | Cash from Operations ÷ Net Sales | 34% | Efficient cash generation |

| Free Cash Flow | Cash from Operations − CapEx | 48,000 | Cash available for investment |

These ratios provide a quick snapshot of cash health, helping stakeholders make informed financial decisions and plan for sustainable growth.

Cash Flow Statement vs Income Statement

The Cash Flow Statement and the Income Statement are two fundamental financial reports, but they serve different purposes and provide distinct insights into a business. Understanding their differences is crucial for analyzing a company’s financial health.

1. Cash Flow Statement

The cash flow statement shows the actual inflows and outflows of cash during a specific period. It tracks cash generated from operating, investing, and financing activities. This statement helps evaluate a company’s liquidity, its ability to meet short-term obligations, and how cash is used for growth or debt repayment.

Example:

| Activity | Cash (USD) |

|---|---|

| Operating Activities | 68,000 |

| Investing Activities | (15,000) |

| Financing Activities | 15,000 |

| Net Increase in Cash | 68,000 |

2. Income Statement

The income statement, also called the profit and loss statement, reports a company’s revenues, expenses, and net profit over a period. It measures profitability rather than actual cash movement and includes non-cash items like depreciation and accruals.

Example:

| Particulars | Amount (USD) |

|---|---|

| Revenue | 200,000 |

| Expenses | 140,000 |

| Net Profit | 60,000 |

Key Differences:

| Feature | Cash Flow Statement | Income Statement |

|---|---|---|

| Focus | Cash inflows and outflows | Revenue, expenses, profit |

| Non-Cash Items | Excluded | Included (e.g., depreciation) |

| Purpose | Liquidity and cash management | Profitability assessment |

| Sections/Components | Operating, Investing, Financing | Revenue, Cost, Expenses, Profit |

Conclusion: While the income statement shows whether a company is profitable, the cash flow statement reveals whether it has enough cash to operate and grow. Both reports together give a complete picture of financial health and help in making informed business decisions.

Common Mistakes in Cash Flow Statement

A Cash Flow Statement is critical for understanding a company’s liquidity, operational efficiency, and financial stability. However, errors during its preparation can lead to misleading conclusions and poor decision-making. Below are some common mistakes businesses often make:

1. Confusing Cash and Profit

Many assume that net profit equals cash available, but income statements include non-cash items like depreciation or accrued expenses. Overlooking these can give a false sense of liquidity.

Example:

Net profit = $60,000, but depreciation = $10,000 and accounts receivable increased by $5,000. Ignoring these adjustments misrepresents actual cash.

2. Misclassifying Cash Flows

Operating, investing, and financing activities must be clearly separated. For instance, issuing shares should be financing, not operating, and buying machinery should be investing. Misclassification affects analysis and ratios.

3. Ignoring Non-Cash Transactions

Transactions like asset swaps, stock dividends, or depreciation do not involve cash but must be adjusted in the statement. Failing to account for these can distort cash flow from operations.

4. Omitting Changes in Working Capital

Changes in accounts receivable, accounts payable, and inventory directly affect cash flow. Not including them leads to inaccurate operating cash flow calculations.

5. Mathematical and Reconciliation Errors

Incorrect addition of inflows and outflows or failing to reconcile opening and closing cash balances is a common technical mistake.

6. Using Inconsistent Methods

Switching between the direct and indirect methods mid-preparation creates confusion and reduces comparability.

Conclusion:

Accurate cash flow statements require careful attention to cash vs profit, correct classification, non-cash adjustments, working capital changes, and reconciliation. Avoiding these mistakes ensures reliable financial analysis, better decision-making, and improved liquidity management.

Tips to Improve Cash Flow Management

Effective cash flow management is essential for the financial health and sustainability of any business. Proper management ensures the company can meet obligations, invest in growth, and avoid liquidity crises. Here are key strategies to improve cash flow:

1. Monitor Cash Flow Regularly

Track inflows and outflows weekly or monthly to detect trends, identify potential shortfalls, and plan ahead. Maintaining a cash flow forecast helps anticipate periods of high or low liquidity.

Example: A business notices seasonal slowdowns in sales. By forecasting cash needs, it arranges short-term financing in advance to cover expenses.

2. Speed Up Receivables

Encourage timely payments from customers by offering early payment discounts or tightening credit terms. Reducing accounts receivable increases cash availability.

3. Control Expenses

Review and categorize expenses regularly. Cut unnecessary costs and negotiate better terms with suppliers to manage outflows efficiently.

4. Manage Inventory Efficiently

Excess inventory ties up cash. Implementing just-in-time inventory or analyzing turnover ratios ensures stock levels match demand without blocking cash.

5. Optimize Financing and Debt

Use short-term financing wisely and refinance high-interest debt to improve cash flow. Avoid over-reliance on credit to cover operational gaps.

6. Plan for Tax Obligations and Contingencies

Set aside cash for taxes, unexpected repairs, or emergencies to prevent sudden liquidity shortages.

7. Invest in Cash Flow Tools

Use accounting software or cash flow management tools to automate tracking, forecasting, and reporting for accurate decision-making.

Summary Table of Key Tips

| Tip | Benefit |

|---|---|

| Monitor cash flow regularly | Anticipate shortages & plan ahead |

| Speed up receivables | Increase liquidity |

| Control expenses | Reduce unnecessary outflows |

| Manage inventory efficiently | Avoid cash being tied in stock |

| Optimize financing | Lower interest costs & improve cash |

| Plan for taxes & contingencies | Avoid unexpected cash shortages |

Implementing these strategies ensures a company maintains steady liquidity, meets obligations on time, and supports growth, making cash flow management a core component of financial success.

Limitations of Cash Flow Statement

The Cash Flow Statement is a vital financial report that shows the movement of cash in a business, helping assess liquidity, operational efficiency, and financing activities. However, like any financial tool, it has certain limitations that users should be aware of:

1. Ignores Profitability

A cash flow statement does not reflect the company’s profitability. A business may have strong cash inflows but could still be unprofitable due to high expenses or declining revenues.

Example: A company receives $100,000 in cash from customers but has $120,000 in total expenses. Cash is positive, but the business is running at a loss.

2. Excludes Non-Cash Transactions

Important non-cash transactions like depreciation, amortization, or stock dividends are excluded. While cash is tracked, these transactions can significantly impact long-term financial health but are not reflected.

3. Limited Predictive Value

The statement shows historical cash flows, not future cash availability. It may not accurately predict future liquidity, especially in businesses with fluctuating sales or seasonal trends.

4. No Assessment of Overall Financial Position

Cash flow alone cannot determine solvency or overall financial strength. Other financial statements, such as the balance sheet and income statement, are needed for a complete assessment.

5. Possibility of Manipulation

Timing of cash receipts and payments can be adjusted to make cash flows appear stronger temporarily. This can mislead stakeholders if not carefully analyzed.

6. Complexity in Preparation

For large businesses, tracking cash flows from multiple operations, investments, and financing activities can be complex and prone to errors if internal controls are weak.

Conclusion:

While the cash flow statement is invaluable for understanding liquidity and cash management, it should be used alongside other financial statements for a comprehensive view of a company’s financial health. Awareness of these limitations ensures better analysis and informed decision-making.

FAQs

1. What is a cash flow statement?

A cash flow statement is a financial report that shows how cash enters and leaves a business over a period. It includes operating, investing, and financing activities and helps assess liquidity and cash management.

2. Why is the cash flow statement important?

It provides insight into a company’s ability to generate cash, pay debts, invest, and fund operations, which cannot be determined from the income statement alone.

3. What are the methods of preparing a cash flow statement?

There are two main methods:

- Direct Method: Records actual cash receipts and payments.

- Indirect Method: Starts with net profit and adjusts for non-cash transactions and working capital changes.

4. What is the difference between cash flow statement and income statement?

The income statement measures profitability, including non-cash items, while the cash flow statement shows actual cash movement during the period, focusing on liquidity.

5. How can I improve cash flow in my business?

Key strategies include monitoring cash flow regularly, speeding up receivables, controlling expenses, managing inventory efficiently, and planning for taxes and contingencies.

6. What are the limitations of a cash flow statement?

It ignores profitability, excludes non-cash transactions, has limited predictive value, and may be complex or manipulated, so it should be used with other financial statements.

7. What are the key cash flow ratios?

Common ratios include:

- Operating Cash Flow Ratio = Cash from operations ÷ Current liabilities

- Cash Flow to Sales Ratio = Cash from operations ÷ Net sales

- Free Cash Flow = Cash from operations − Capital expenditures

8. Can a company have profit but negative cash flow?

Yes. Profit includes non-cash items and accruals, so a company can be profitable on paper but have negative cash flow due to high receivables, inventory, or debt payments.

9. How often should a cash flow statement be prepared?

Most businesses prepare it monthly, quarterly, or annually, depending on management needs, size, and financial reporting requirements.

10. Can small businesses benefit from cash flow statements?

Absolutely. Even small businesses can use cash flow statements to track liquidity, plan expenses, and avoid cash shortages.

Conclusion

The Cash Flow Statement is one of the most important financial statements for any business, providing a clear picture of how cash moves in and out of the organization. Unlike the income statement, which focuses on profits, the cash flow statement highlights actual cash availability, making it a critical tool for liquidity management, investment decisions, and financial planning.

By analyzing cash flows from operating, investing, and financing activities, businesses can identify strengths and weaknesses in their cash management. For example, strong operating cash flow indicates that core operations generate sufficient cash, while significant investing outflows may signal growth initiatives or asset expansion. Financing activities, on the other hand, reveal how a business funds its operations and growth through debt, equity, or dividends.

Despite its usefulness, the cash flow statement has limitations. It does not show profitability, ignores non-cash transactions, and cannot fully predict future cash flows. Therefore, it should be used alongside the income statement and balance sheet to get a complete view of a company’s financial health.

Practical applications such as cash flow ratio analysis, monitoring receivables and payables, and planning for contingencies help management make informed decisions and maintain healthy liquidity. Companies that pay attention to cash flow are better equipped to handle unexpected expenses, capitalize on opportunities, and sustain long-term growth.

In summary, a well-prepared cash flow statement not only tracks cash movements but also acts as a strategic tool for financial decision-making, operational efficiency, and risk management. Businesses that understand and actively manage their cash flow can maintain stability, improve profitability, and build confidence among investors and stakeholders.