{kind=link}

Introduction to Cost of Capital

Every business needs money to grow, whether it comes from loans or investors. The cost of capital is the price a company pays to use that money. It represents the minimum return a business must earn on its investments to satisfy lenders and shareholders. If a company earns less than this required return, it may struggle to create value.

There are two main sources of capital. One is debt, such as bank loans or bonds, where the company pays interest. The other is equity, where investors provide funds in exchange for ownership and expect returns through dividends or rising share value. Each source has its own cost, and companies must carefully balance both.

Think of cost of capital as a benchmark for decision making. Before investing in a project, businesses compare expected returns with their cost of capital. If the return is higher, the project is worth considering. If not, it may lead to losses over time.

Example:

A company raises funds at an average cost of 10 percent. If it invests in a project that generates a return of 14 percent, it creates value. But if the return is only 8 percent, the company is effectively losing money.

Key points to remember:

• It reflects the risk level of a business

• It helps in making investment decisions

• It plays a major role in determining a company’s value and growth

Understanding the cost of capital is essential for anyone studying finance or running a business, as it forms the foundation for smarter financial planning and long term success.

What is Cost of Debt?

The cost of debt is the effective rate of interest a company pays on the money it borrows from lenders such as banks, financial institutions, or bondholders. It represents the actual cost a business incurs for using borrowed funds to finance its operations or investments.

When a company takes a loan or issues bonds, it agrees to pay interest at a fixed or variable rate. This interest becomes the cost of debt. However, one important advantage is that interest payments are usually tax-deductible, which reduces the overall cost to the company.

In simple terms, cost of debt tells us how expensive it is for a business to rely on borrowing instead of using its own funds.

Example:

Suppose a company takes a loan of $100,000 at an interest rate of 8 percent. The annual interest paid will be $8,000, which represents the cost of debt before tax. If the company benefits from tax deductions, the actual cost becomes lower.

Key highlights:

• It is generally cheaper than equity financing

• Interest payments are fixed and predictable

• It provides a tax advantage due to deductibility

• Higher debt increases financial risk

Understanding the cost of debt is important because it helps businesses decide how much borrowing is suitable and how it affects overall profitability and financial stability.

Formula for Cost of Debt

The cost of debt is calculated to understand how much a company actually pays for its borrowed funds. It can be measured in two ways, before tax and after tax, but in practice, businesses focus more on the after tax cost because of the tax benefit on interest.

1. Pre Tax Cost of Debt

This formula shows the basic interest rate a company pays on its borrowings.

Example:

If a company pays $5,000 in annual interest on a loan of $50,000, the cost of debt is 10 percent.

2. After Tax Cost of Debt

Where

r_d is the interest rate on debt

T is the corporate tax rate

This formula reflects the tax advantage, since interest expenses reduce taxable income.

Example:

If the interest rate is 10 percent and the tax rate is 30 percent, then:

After tax cost = 10 percent × (1 − 0.30) = 7 percent

Key points to remember:

• After tax cost is more realistic for decision making

• Debt is usually cheaper than equity due to tax savings

• Useful in calculating overall cost of capital

Understanding these formulas helps businesses evaluate borrowing decisions and manage their financing strategy more effectively.

Advantages of Cost of Debt

Using debt as a source of finance offers several practical benefits for businesses, especially when managed carefully.

1. Tax Advantage

Interest payments are tax-deductible, which reduces the company’s taxable income. This makes debt a cheaper source of financing compared to equity.

2. Lower Cost Compared to Equity

Debt usually carries a lower cost because lenders take less risk than shareholders. This helps companies reduce their overall cost of capital.

3. No Ownership Dilution

Borrowing money does not require giving up ownership. The company retains full control, unlike equity financing where shares are issued.

4. Predictable Payments

Interest payments are fixed and scheduled, making it easier for businesses to plan cash flows and budgets.

5. Enhances Returns

If used wisely, debt can improve returns to shareholders through financial leverage, especially when investments generate higher returns than the interest cost.

Disadvantages of Cost of Debt

Despite its benefits, debt financing also brings certain risks that businesses must consider.

1. Fixed Financial Obligation

Interest must be paid regularly, regardless of whether the company is making a profit or not. This can create pressure during low revenue periods.

2. Increased Financial Risk

High levels of debt increase the risk of default or bankruptcy, especially if cash flows are unstable.

3. Impact on Credit Rating

Too much borrowing can negatively affect a company’s creditworthiness, making future borrowing more expensive or difficult.

4. Collateral Requirement

Lenders often require assets as security, which puts company assets at risk if repayments are not made.

5. Limited Flexibility

Debt agreements may include restrictions or covenants, limiting business decisions such as expansion or dividend payments.

A balanced approach is important. While debt can be a powerful tool for growth, excessive reliance on it can weaken financial stability.

What is Cost of Equity?

The cost of equity is the return that shareholders expect for investing their money in a company. Unlike debt, where interest payments are fixed, equity investors take on higher risk, so they expect a higher return as compensation.

When a company raises funds by issuing shares, it does not have to repay the money like a loan. However, it is still “costly” because investors expect profits in the form of dividends and capital gains. If the company fails to deliver these returns, investors may lose confidence and the share price can fall.

In simple terms, the cost of equity is what a company must earn to keep its investors satisfied and willing to continue investing.

Example:

If investors expect a return of 12 percent on their investment in a company, then 12 percent becomes the cost of equity. Any project the company undertakes should aim to generate at least this level of return.

Key highlights:

• It is usually higher than the cost of debt due to higher risk

• There is no fixed obligation to pay dividends

• It leads to ownership dilution when new shares are issued

• It reflects investor expectations and market conditions

Understanding the cost of equity is crucial because it helps businesses evaluate investment opportunities and maintain a balance between risk and return while making financing decisions.

Formula for Cost of Equity

The cost of equity represents the return that investors expect for putting their money into a company. Since there is no fixed interest like debt, it is calculated using financial models that estimate expected returns based on dividends or market risk.

There are two widely used methods to calculate the cost of equity:

1. Dividend Discount Model (DDM)

Where

rₑ is the cost of equity

D₁ is the expected dividend next year

P₀ is the current share price

g is the growth rate of dividends

This method works best for companies that regularly pay dividends.

Example:

If a company’s share price is $100, expected dividend is $5, and growth rate is 4 percent, then:

Cost of equity = 5/100 + 0.04 = 9 percent

2. Capital Asset Pricing Model (CAPM)

Where

rₑ is the cost of equity

r_f is the risk free rate

β measures risk compared to the market

r_m is the market return

This method focuses on risk and market performance, making it more widely used in practice.

Example:

If risk free rate is 3 percent, beta is 1.2, and market return is 10 percent, then:

Cost of equity = 3% + 1.2 × (10% − 3%) = 11.4 percent

Key points to remember:

• Cost of equity is usually higher than cost of debt

• It reflects investor expectations and risk level

• CAPM is more commonly used for modern financial analysis

Understanding these formulas helps businesses choose the right investment opportunities and maintain a balance between risk and return.

Advantages of Cost of Equity

Equity financing provides businesses with flexibility and stability, especially in uncertain conditions. Although it may seem expensive, it offers several long term benefits.

1. No Repayment Obligation

Unlike debt, equity does not require fixed repayments. This reduces financial pressure, especially when profits are low.

2. Lower Financial Risk

Since there are no mandatory interest payments, the risk of bankruptcy or default is much lower compared to borrowing.

3. Flexibility in Returns

Dividends are not compulsory. Companies can adjust or skip them based on performance, which helps in managing cash flow effectively.

4. Strong Financial Position

Raising equity improves the company’s balance sheet strength, making it easier to attract future investment or financing.

5. Long Term Capital Source

Equity provides funds that stay in the business for the long term, supporting growth and expansion without immediate pressure.

Disadvantages of Cost of Equity

Despite its advantages, equity financing also has some important drawbacks that businesses must consider.

1. Higher Cost

Equity is generally more expensive because investors expect higher returns due to higher risk.

2. Ownership Dilution

Issuing new shares reduces the ownership percentage of existing shareholders, leading to loss of control.

3. Profit Sharing

Profits must be shared with shareholders in the form of dividends, which reduces retained earnings.

4. Investor Expectations

Equity investors often expect strong performance and growth, which can create pressure on management.

5. Complex and Time Consuming Process

Raising equity involves legal procedures, valuations, and regulatory requirements, making it more complex than borrowing.

A smart financing strategy often combines both debt and equity to balance risk, cost, and control, ensuring sustainable business growth.

Practical Example: Cost of Debt vs Equity

Understanding the difference between the cost of debt and the cost of equity becomes clearer with a simple real world style example.

Imagine a company needs $100,000 to expand its operations. It has two options, borrow money or raise funds from investors.

If the company chooses debt financing, a bank offers a loan at an interest rate of 10 percent. However, interest is tax deductible. If the corporate tax rate is 30 percent, the actual cost becomes lower.

After tax cost of debt

So the effective cost is

10% × (1 − 0.30) = 7 percent

Now consider equity financing. Investors expect a return of 15 percent because they take more risk. Unlike debt, there are no tax benefits, and returns are not guaranteed.

Comparison in this case

- Cost of debt is 7 percent after tax

- Cost of equity is 15 percent

- Debt appears cheaper, but it comes with fixed repayment obligations

- Equity is expensive, but it reduces financial pressure

What this means in practice

If the company uses more debt, it lowers its overall cost of capital, but increases financial risk. Missing interest payments can lead to serious consequences. On the other hand, relying more on equity keeps the company safer during tough times, but reduces profits available to owners.

Key takeaway

- Debt is cheaper but risky due to fixed commitments

- Equity is costly but flexible with no mandatory payments

- A smart business finds a balance based on its stability and growth stage

In real business decisions, companies rarely choose one over the other. Instead, they combine both to create a capital structure that supports growth while managing risk effectively.

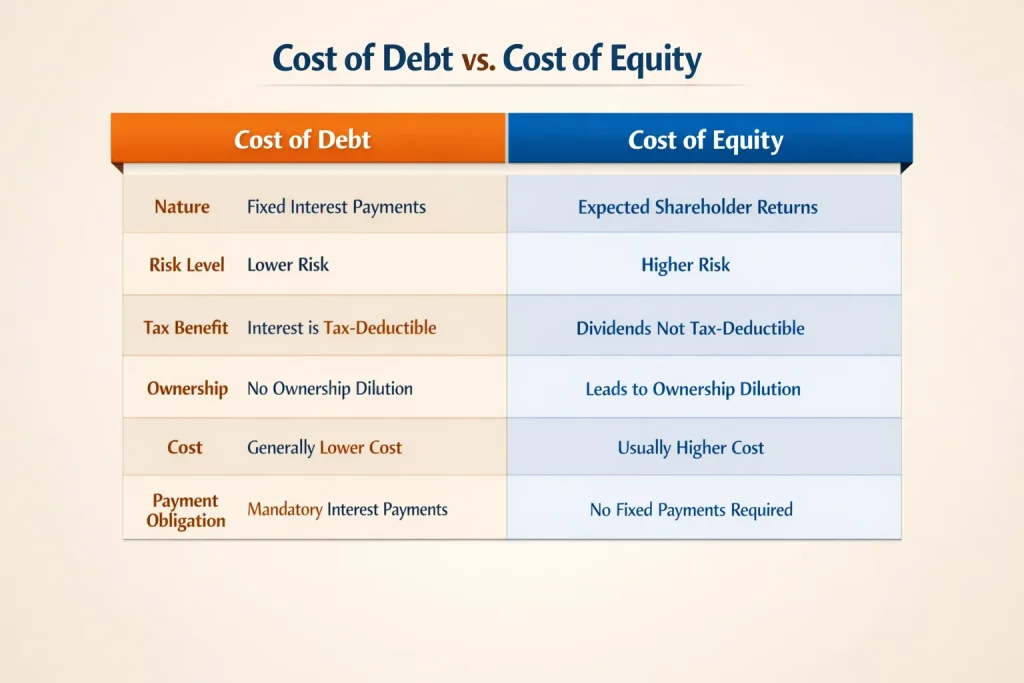

Key Differences Between Cost of Debt and Cost of Equity

Understanding the difference between cost of debt and cost of equity is essential for making smart financial decisions. Both are sources of funding, but they behave very differently in terms of risk, return, and impact on a business.

The cost of debt is the interest a company pays on borrowed funds, while the cost of equity is the return expected by investors who own shares in the company. This basic distinction leads to several important differences.

1. Risk Level

Debt is generally less risky for investors because lenders receive fixed interest payments. Equity investors face higher uncertainty, so the cost of equity is usually higher.

2. Return Expectation

Debt holders earn fixed returns, while equity investors expect variable and often higher returns through dividends and capital appreciation.

3. Tax Treatment

Interest on debt is tax-deductible, which reduces the overall cost. In contrast, dividends paid to shareholders are not tax-deductible, making equity more expensive.

4. Ownership and Control

Debt financing does not affect ownership. Equity financing leads to ownership dilution, as new shareholders gain a stake in the company.

5. Payment Obligation

Debt requires mandatory interest payments, regardless of profit. Equity does not require fixed payments, as dividends depend on company performance.

6. Impact on Financial Risk

Higher debt increases financial risk due to repayment obligations. Equity reduces financial pressure but may increase expectations from investors.

Simple comparison example:

A company borrows funds at 8 percent interest but raises equity where investors expect 14 percent return. Debt appears cheaper, but too much borrowing can increase financial risk, while equity provides flexibility but at a higher cost.

In practice, businesses use a mix of both to balance cost, risk, and control, ensuring long term financial stability and growth.

Cost of Debt vs Cost of Equity: Side-by-Side Comparison

| Aspect | Cost of Debt | Cost of Equity |

|---|---|---|

| Definition | Interest a company pays on borrowed funds | Return expected by shareholders for investing in the company |

| Risk | Lower risk for investors; fixed interest payments | Higher risk for investors; returns depend on performance |

| Return | Fixed and predictable | Variable; includes dividends and capital gains |

| Tax Treatment | Interest is tax-deductible, reducing effective cost | Dividends are not tax-deductible |

| Ownership Impact | No ownership dilution | Leads to ownership dilution when new shares are issued |

| Payment Obligation | Mandatory interest payments regardless of profit | Dividends are discretionary; not mandatory |

| Financial Risk | High debt increases financial risk | Equity reduces financial risk but increases pressure for growth |

| Cost | Generally lower than equity | Usually higher due to higher risk |

| Usefulness | Effective for short-term funding and leveraging | Ideal for long-term growth and capital stability |

| Example | Loan at 8% interest per year | Shareholders expect 12% return per year |

This table makes it clear why companies carefully balance debt and equity in their capital structure to minimize cost while managing risk.

Role in Capital Structure Decisions

Capital structure decisions shape how a business finances its operations through a mix of debt and equity. The role of these decisions is not just about raising funds, but about finding the right balance that supports growth while controlling risk and cost.

At the core, managers aim to minimize the cost of capital and maximize the value of the firm. Debt is often cheaper because of tax benefits, but too much borrowing increases financial risk. Equity is safer in terms of repayment pressure, yet it can dilute ownership and control. The decision lies in choosing a structure that aligns with the company’s long term strategy.

A key role of capital structure decisions is managing financial risk. Higher debt leads to fixed obligations like interest payments, which can strain cash flow during downturns. On the other hand, a well balanced mix improves financial stability and investor confidence.

Another important aspect is flexibility. Companies need room to adapt to market changes. A firm with excessive debt may struggle to raise additional funds when new opportunities arise.

Example

A growing startup may rely more on equity to avoid repayment pressure. In contrast, a stable company with predictable cash flows, such as a manufacturing firm, may use more debt to benefit from lower costs.

Key roles include

- Optimizing cost of capital to improve profitability

- Balancing risk and return for shareholders

- Maintaining control and ownership structure

- Ensuring financial flexibility for future investments

In essence, capital structure decisions act as a financial foundation. A thoughtful approach can drive sustainable growth, while poor choices may lead to financial stress or even business failure.

Weighted Average Cost of Capital (WACC)

The Weighted Average Cost of Capital (WACC) represents the average rate a company pays to finance its business through a mix of debt and equity. It reflects the minimum return a company must earn on its investments to satisfy its investors and lenders.

At its essence, WACC combines the cost of each financing source based on its proportion in the overall capital structure.

Where

E is equity, D is debt, and V is total capital

Re is cost of equity, Rd is cost of debt

T is corporate tax rate

WACC plays a crucial role in financial decision making. It acts as a benchmark for evaluating investment opportunities. If a project’s return is higher than WACC, it adds value to the company. If it falls below, it may destroy value.

One of the key roles of WACC is in capital budgeting. Businesses use it as a discount rate to calculate present value in methods like net present value. It also helps in assessing risk, since a higher WACC often indicates higher perceived risk by investors.

Example

Suppose a company finances itself with 60 percent equity and 40 percent debt. If the cost of equity is 12 percent and the cost of debt is 8 percent with a tax rate of 25 percent, the WACC will be lower than 12 percent due to the tax advantage on debt. This makes borrowing an attractive option up to a certain level.

Key insights

- Measures overall cost of financing

- Used to evaluate investments and projects

- Helps balance debt and equity decisions

- Impacts company valuation and growth strategy

In simple terms, WACC is the financial heartbeat of a company. It tells whether the business is creating value or just covering its cost of capital.

When Should a Company Choose Debt vs Equity?

Choosing between debt and equity is not a one size decision. It depends on the company’s financial position, growth stage, and risk tolerance. The goal is to select the option that supports growth without putting unnecessary pressure on the business.

A company should consider debt financing when it has stable and predictable cash flows. Regular income makes it easier to handle fixed interest payments. Debt is also attractive when interest rates are low, since it reduces the overall cost of capital. Another advantage is that owners retain full control, as lenders do not gain ownership.

Debt is suitable when

- The business has consistent cash flow

- The company wants to retain ownership control

- Interest rates are relatively low

- The firm can benefit from tax savings on interest

On the other hand, equity financing is better when the business faces uncertainty or is in an early growth stage. Startups and expanding companies often prefer equity because it does not require fixed repayments. This reduces financial stress, especially when revenues are not yet stable.

Equity is suitable when

- Cash flows are uncertain or fluctuating

- The company is in a startup or expansion phase

- The business wants to avoid debt burden

- There is a need for strategic investors who can add value

Example

A new tech startup with unpredictable revenue will likely raise equity from investors. In contrast, a well established manufacturing firm with steady sales may rely more on debt to finance expansion at a lower cost.

Final insight

The smartest approach is rarely choosing only one option. Successful companies focus on a balanced capital structure, using debt to reduce costs and equity to maintain flexibility. The right mix helps the business grow confidently while keeping financial risk under control.

Common Mistakes to Avoid in Capital Structure Decisions

Making the right financing choice is critical, yet many businesses fall into avoidable traps. These mistakes often lead to higher costs, financial stress, or missed growth opportunities.

One common error is relying too heavily on cheap debt without considering risk. While debt may look attractive due to lower cost and tax benefits, excessive borrowing can create pressure through fixed interest payments. When cash flow weakens, this becomes a serious burden.

Another mistake is ignoring the true cost of equity. Many assume equity is free because there are no mandatory payments. In reality, investors expect high returns, and giving away ownership can reduce long term value for existing owners.

Poor understanding of business risk is also a major issue. Companies with unstable revenue sometimes take on debt they cannot comfortably manage. This mismatch between risk and financing choice often leads to financial distress.

Key mistakes include

- Overleveraging the business with too much debt

- Ignoring dilution and control loss in equity financing

- Not aligning financing with cash flow stability

- Focusing only on short term cost instead of long term impact

Another overlooked problem is lack of financial flexibility. Companies that use up all borrowing capacity may struggle to raise funds when new opportunities arise. This limits growth and strategic decision making.

Example

A small business takes a large loan to expand quickly, assuming future sales will cover repayments. When demand drops, the company struggles to meet interest payments, leading to cash flow problems. A balanced mix of debt and equity could have reduced this risk.

Final thought

Avoiding these mistakes requires a clear understanding of both cost and risk. Smart capital structure decisions are not about choosing the cheapest option, but about building a sustainable financial foundation that supports long term success.

FAQs on Cost of Debt vs Equity

1. What is the main difference between cost of debt and cost of equity?

The cost of debt is the interest a company pays on borrowed funds, usually adjusted for tax benefits. The cost of equity is the return investors expect for taking ownership risk. Debt involves fixed payments, while equity returns depend on business performance.

2. Why is debt usually cheaper than equity?

Debt is often cheaper because of tax deductibility of interest and lower risk for lenders. In case of liquidation, lenders are paid before shareholders, which reduces their risk and required return.

3. Is equity always safer than debt?

Equity is safer in terms of cash flow pressure since there are no mandatory payments. However, it can be risky for owners because it involves ownership dilution and sharing future profits.

4. How does business size affect the choice?

Smaller or growing businesses often prefer equity due to uncertain cash flows. Larger, stable companies tend to use more debt because they can handle regular interest payments more comfortably.

5. Can a company rely only on debt or only on equity?

In theory yes, but in practice it is not ideal. Using only debt increases financial risk, while relying only on equity can be expensive. Most companies use a balanced mix to optimize cost and flexibility.

6. How do interest rates impact the decision?

When interest rates are low, debt becomes more attractive. When rates rise, companies may shift toward equity to avoid higher borrowing costs.

7. Does industry type matter?

Yes. Capital intensive industries like manufacturing often use more debt, while technology or startups rely more on equity due to higher uncertainty.

8. What is the key takeaway?

There is no perfect choice. The best decision depends on cash flow stability, growth stage, and risk tolerance. A thoughtful balance between debt and equity helps businesses grow while staying financially secure.

Conclusion

The choice between cost of debt and cost of equity is not about picking the cheaper option, but about understanding how each source of finance affects the overall health of a business. Debt offers the advantage of lower cost and tax benefits, yet it brings fixed obligations that can strain cash flow. Equity, on the other hand, provides flexibility and reduces financial pressure, but comes at the cost of higher expected returns and shared ownership.

A well managed company does not rely entirely on one source. Instead, it focuses on creating a balanced capital structure that aligns with its risk level, growth plans, and financial stability. The right mix helps reduce the overall cost of capital while maintaining enough flexibility to handle uncertainty and seize new opportunities.

In practice, strong financial decisions come from evaluating both risk and return together. Businesses that understand this balance are better positioned to grow sustainably, protect themselves during downturns, and maximize long term value for stakeholders.